Many entrepreneurs we work with pride themselves on having no debt on their books and for them, that’s awesome! Hey, borrowing money can feel stressful for sure. For those looking for capital to grow their business and prefer not to sell equity, debt can be a very smart and relatively inexpensive form of financing.

But how much can your company borrow? This article explains a couple of ways you can to analyze how much you can borrow before shopping for potential lending sources.

There Are Many Paths

There’s a lot of flexible capital in the market today to meet the lending financing needs of small business owners, and it’s worth understanding the options. Here’s a brief primer:

- Bank loans: Banks loan via lines of credit (ability to draw and payback dynamically) or term loans (fixed amounts repayable over time). These tend to be the most conservative and most inexpensive options.

- Revenue loans: These are loans against future revenue where the payback is based on a percentage of revenue. A good resource to learn more about this is Lighter Capital.

- High yield loans: These loans are typically non-traditional, meaning they’re not administered through a bank, and are more costly. There are online companies today, like Kabbage, creating viable paths for small loans.

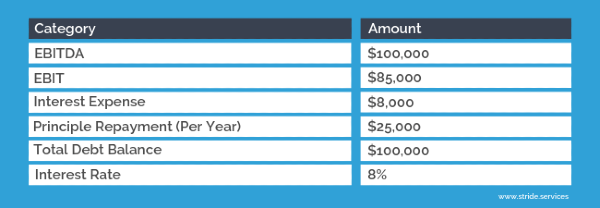

How Much Can You Borrow?

Let’s take a more traditional bank loan, for example. In terms of borrowing, banks often look at two very important ratios: the “Debt Service Coverage Ratio” and the “Interest Coverage Ratio”. These ratios are meant to evaluate the risk of a company who won’t be able to service the debt. Here is how they work…

Debt Service Coverage Ratio (“DSCR”)

The DSCR is calculated as EBITDA (Earnings Before Interest, Tax, and Depreciation) divided by Debt Payments (Principal Repayment + Interest). Essentially, EBITDA (which is calculated from the income statement) is a proxy for cash and lenders generally look for a ratio over 1.2. This means that a Company has 1.2 times the cash available to pay debt principal and interest in a given year.

Interest Coverage Ratio (“ICR”)

The ICR is calculated as EBIT (Earnings Before Interest and Tax) divided by interest expense in a given period. Interest expense represents the cost an owner pays for the outstanding debt. The ratio, which lenders want to be over 2.0x, is a signal of available income to cover interest expense while a loan is outstanding.

Let’s look at an example…

DSCR = $100,000/ ($25,000+$8,000) = 3.0x

ICR = $80,000 / $8,000 = 10x

Okay, this seems like a reasonable level of debt for our example company. But how much borrowing is available? If we set the DSCR at 1.2, the max Principal + Interest would be: $100,000 / 1.2 = $83,333.

Let’s compare that to the $33,000 of current Principal + Interest. We might assume the company could take on 2.5x the level of debt currently in the business (from $100,000 to $250,000). At an 8% interest rate, $250,000 of debt would be $20,000 of interest per year ($250,000 x 8%).

Now let’s look at the ICR. At $20,000 of interest expense per year, the revised ICR would be $85,000/$20,000 = 4.25x which is below that 2.0 threshold.

So, What Should the Company Do? Lead with Strategy!

The good news is we have answered a tactical question about borrowing capacity, such as does the company have the capacity to take on another $150,000 of debt? While the company can support it, this doesn’t mean the business owner should do it. Why? Well, the trick is in understanding how potential financing maps to the company’s strategy. What is the additional capital going toward? What value can the investment create? How cyclical is the business and if it were to stumble, would the company be able to cover its debt obligation? Often these strategic questions drive the financing decisions of debt vs. equity.

While the parameters above are not set in stone for every lender, they are designed to give the business owner a bit better control to understand what is possible based on their current financial position. At Stride, we work with companies to produce consistent, timely and quality financial statements that allow for these calculations to be made efficiently. If you are interested in learning more, please contact us.